Yole Group announces the release of the Status of the Semiconductor Foundry Industry 2026 report. Yole Group’s annual report on the semiconductor foundry industry provides a comprehensive and updated view of the global manufacturing landscape shaping the semiconductor ecosystem.

The foundry report examines the structural transformation currently underway in semiconductor manufacturing. Over the past few years, massive investments have been deployed worldwide to expand fabrication capacity and strengthen regional semiconductor supply chains. At the same time, the rapid expansion of artificial intelligence and high-performance computing is accelerating demand for advanced semiconductor technologies.

The foundry report examines the structural transformation currently underway in semiconductor manufacturing. Over the past few years, massive investments have been deployed worldwide to expand fabrication capacity and strengthen regional semiconductor supply chains. At the same time, the rapid expansion of artificial intelligence and high-performance computing is accelerating demand for advanced semiconductor technologies.

Yole Group’s analyst confirms that the industry is now entering a new phase where advanced-node manufacturing and AI-driven demand are reshaping the competitive landscape.

Published annually, the Status of the Semiconductor Foundry Industry 2026 report tracks the evolution of the semiconductor market, capacity expansion, technology transitions, and competitive positioning across the global foundry ecosystem. It also serves as a benchmark for industry stakeholders seeking to anticipate market shifts, understand supply-chain dynamics, and align their strategies with the next generation of semiconductor manufacturing technologies.

According to Yole Group, in 2025, global semiconductor wafer demand reached 8,700 thousand wafers per month (12’’ equivalent). Analysts expect continuous and steady growth through the end of the decade. Meanwhile, global foundry capacity continues to expand, projected to reach 15,250 thousand wafers per month by 2031. The CAGR should be 4% from 2025 to 2031.

The industry is experiencing a structural imbalance between supply and demand. Following the semiconductor shortages of 2021–2022, large investments in fabrication plants increased manufacturing capacity faster than wafer demand. As a result, global foundry utilization dropped to 73% in 2025, with forecasts indicating utilization may remain between 70% and 75% over the coming years.

Artificial intelligence is currently the primary driver, while the Automotive and Industrial sectors are back to pulling semiconductor demand. The open foundry market rebounded strongly after the 2023 downturn, reaching $181 billion in revenue in 2025, supported by rising demand for advanced nodes used in Artificial Intelligence and high-performance computing chips.

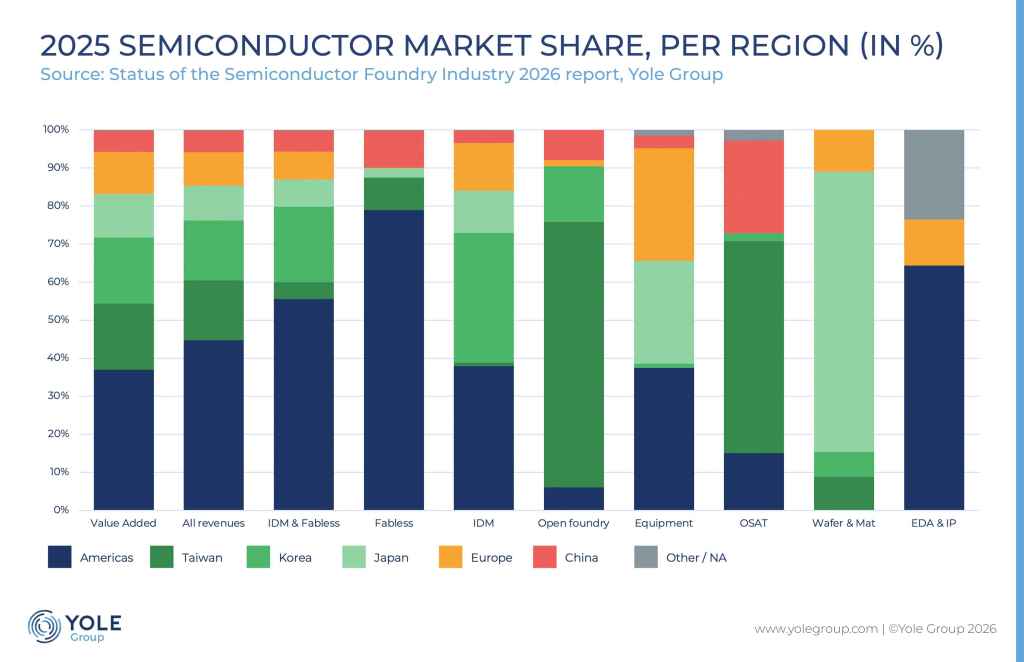

Yole Group’s report also highlights the ongoing transformation of the semiconductor ecosystem. The industry is increasingly structured around the fabless business model, in which semiconductor device companies only design chips while specialized foundries manufacture them. This evolution has reinforced the dominance of major foundry players, particularly TSMC, which increased its market share to approximately 32% of global semiconductor manufacturing and 68% of the open foundry market in 2025.

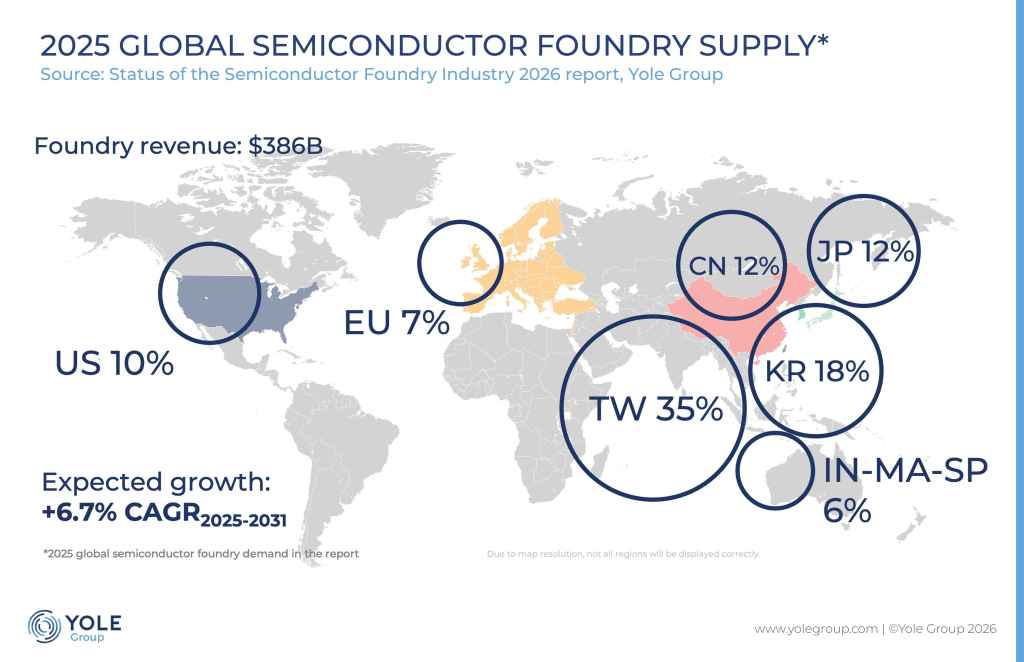

Geographically, semiconductor manufacturing remains strongly concentrated in Asia. Taiwan continues to lead in advanced semiconductor manufacturing, while South Korea remains a major competitor in memory-related technologies. At the same time, mainland China has rapidly expanded its manufacturing footprint and could reach 30% of global foundry capacity by 2031, reflecting sustained investments in domestic semiconductor production.

Further insights into semiconductor industry dynamics will be shared by Yole Group’s President and Founder, Jean-Christophe Eloy, at the Industry Strategy Symposium (ISS) China 2026, where he will discuss equipment trends and investment strategies shaping the next wave of semiconductor manufacturing expansion.